Buy Apple? Best REIT Type?

Buy Apple? Best REIT Type?

Good Morning Dividend Investing Friend!!

Here is the combined Dividend Growth and High Yield report, we should have the new separate services functional for tomorrow.

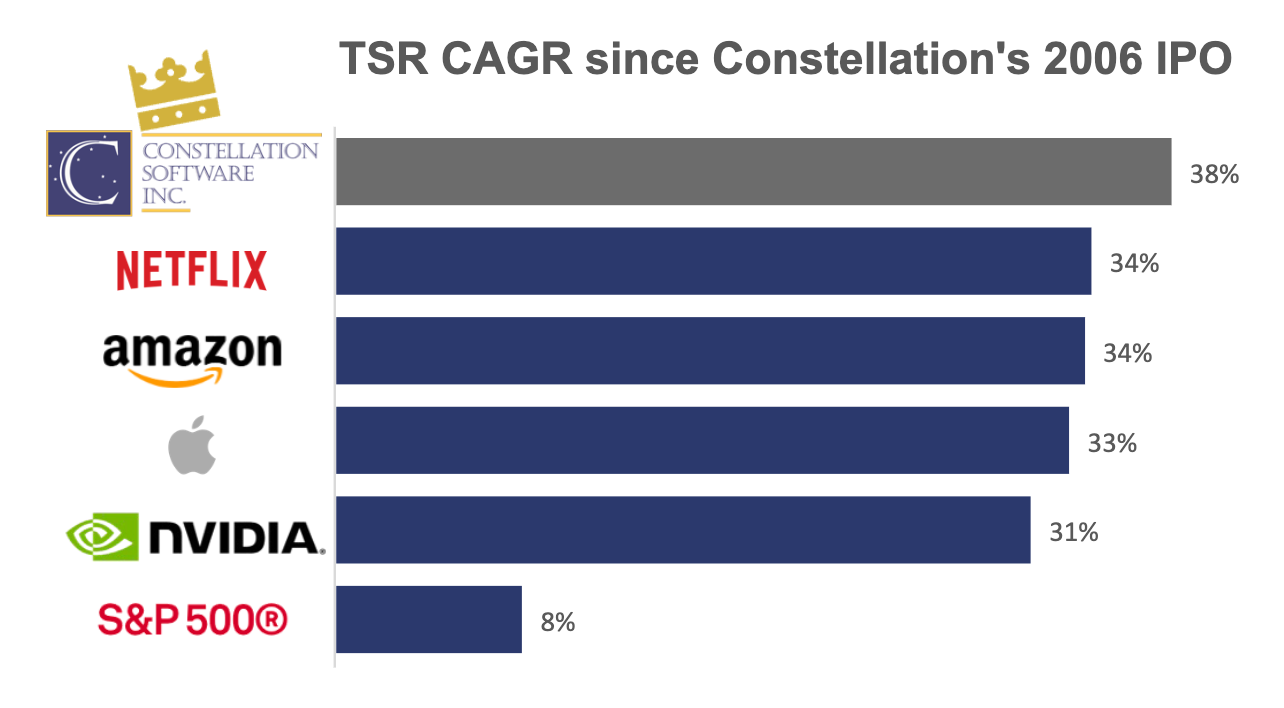

Let’s keep going with Serial Acquirer week!

Yesterday we said that most acquisitions fail, hence the opportunity and good valuations in the acquirers that have gotten the formula right. We also talked about asset-light serial acquirers.

Today we will keep going with these amazing companies, here is the link to this morning’s opening bell show:

https://youtube.com/live/iYmCi70_5fk

Here is what your Dividends Guide says about asset-light companies:

"The best results occur at companies that require minimal assets to conduct high-margin businesses – and offer goods or services that will expand their sales volume with only minor needs for additional capital." – Warren Buffett’s 2020 letter

The more assets you have, the more Maintenance CapEx you might expect to be required for upkeep of those assets. Therefore, companies with fewer assets often have better free cash flows, as they are unencumbered by upkeep costs (Maintenance CapEx reducing FCF). We should place special attention on these asset-light stocks.

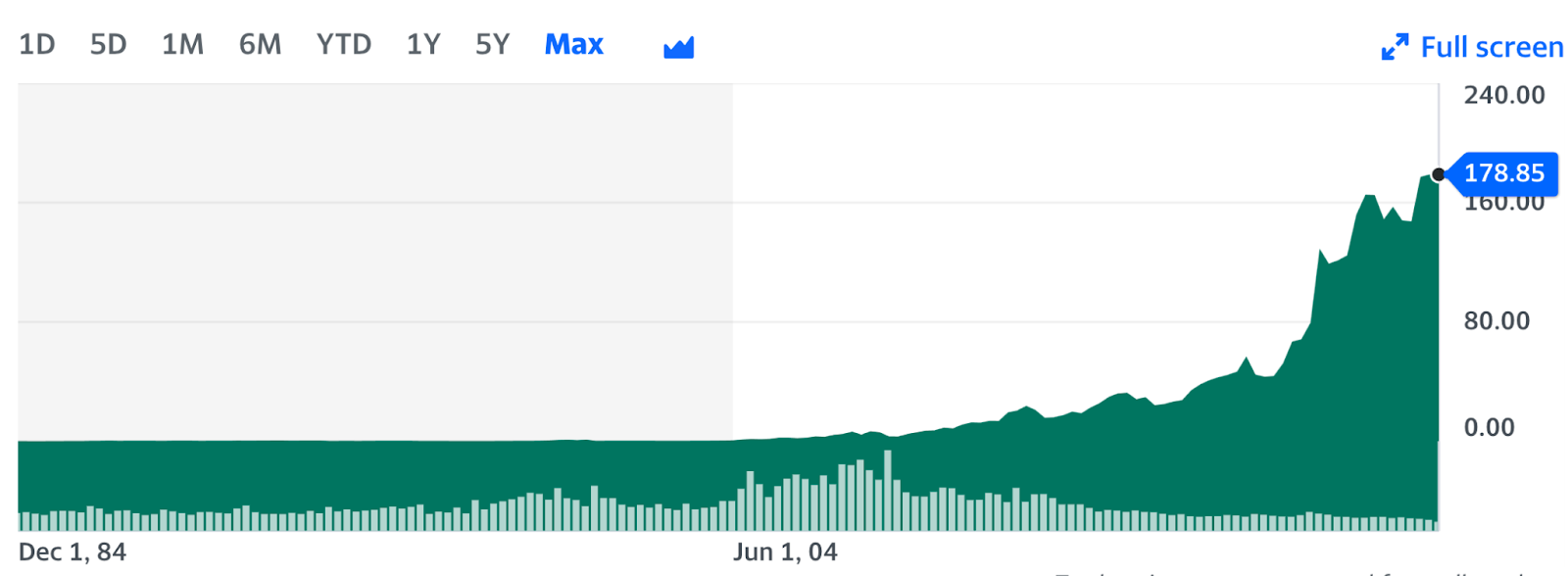

Apple (AAPL) is one such asset-light serial acquirer – with stellar returns:

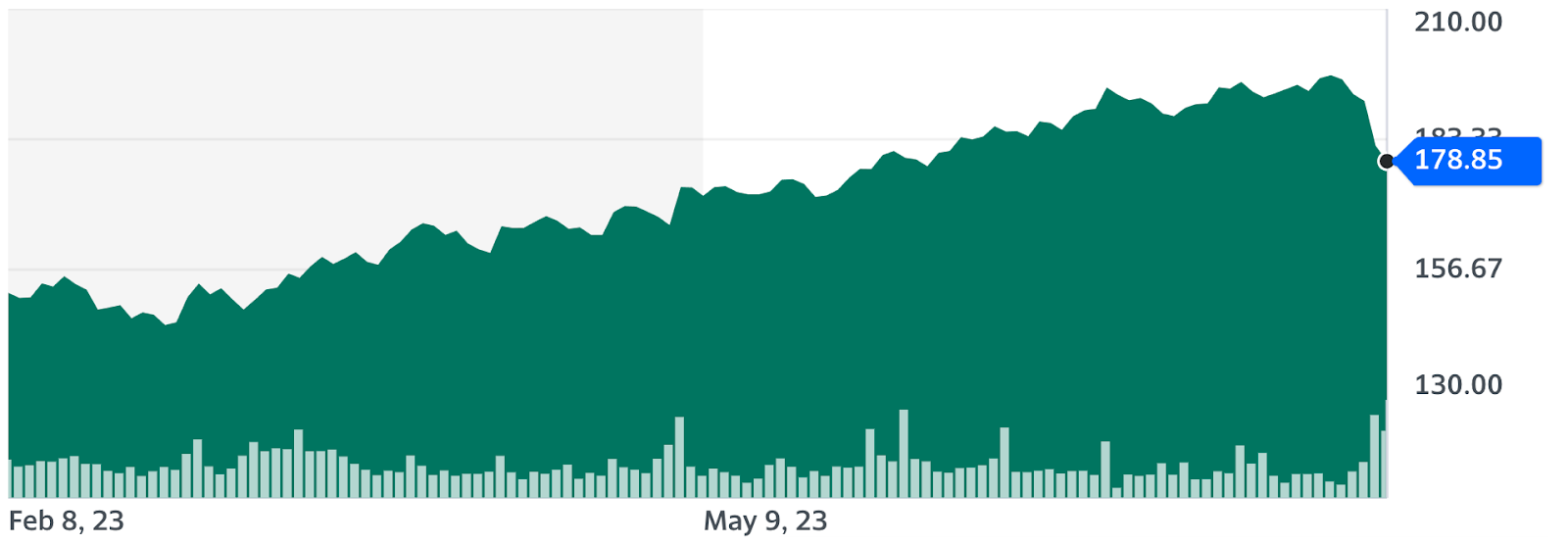

And as Apple is now off 10% from its highs:

Is it time to buy?

Well, FCF/share is looking pretty good, the latest quarter was up 20% year-over-year:

And we know Apple has a couple of terrific moats, from the Dividends Guide again:

How do we know if the FCF good times are sustainable going forward? We look for sustainable competitive advantages, aka moats.

Companies have a moat when they have something special that gives them a sustainable advantage over competitors or new entrants to the market.

Apple, for example, has a massive already-existing network of enthusiastic users, as well as a massive offering of already-existing apps and services in its ecosystem. If Apple decides to roll out a new offering, millions are waiting to buy – that is a nearly insurmountable advantage over any new entrant looking to do what Apple is doing. And once users are in the ecosystem, they have all of their media and information that would be lost if they left – they are captive customers.

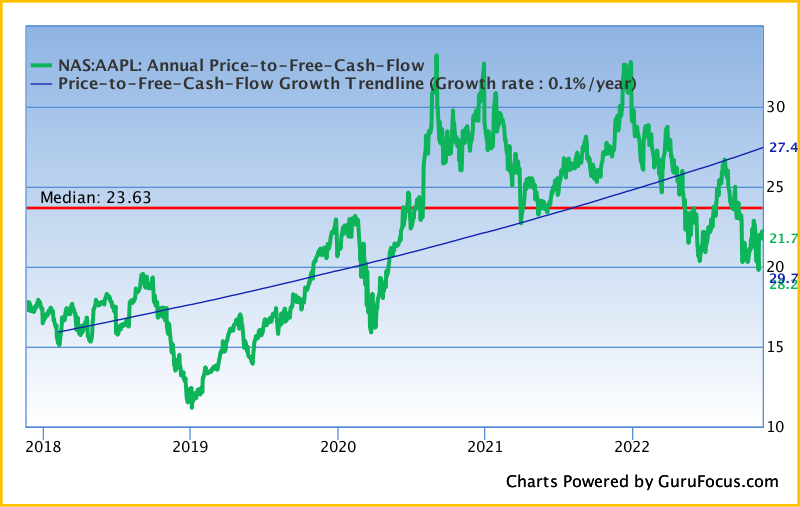

And Apple is not too overvalued on its FCF/share relative to its post-COVID valuations. Currently its Price-to-FCF/Share is 28.19.

That metric has been over 30 lately, and considering the healthy 20% growth and recent 10% discount…